.png)

Weekly Reflection for March 10, 2023

- Serene Point

- Mar 10, 2023

- 5 min read

Updated: May 30, 2025

The Week - An Update in Charts

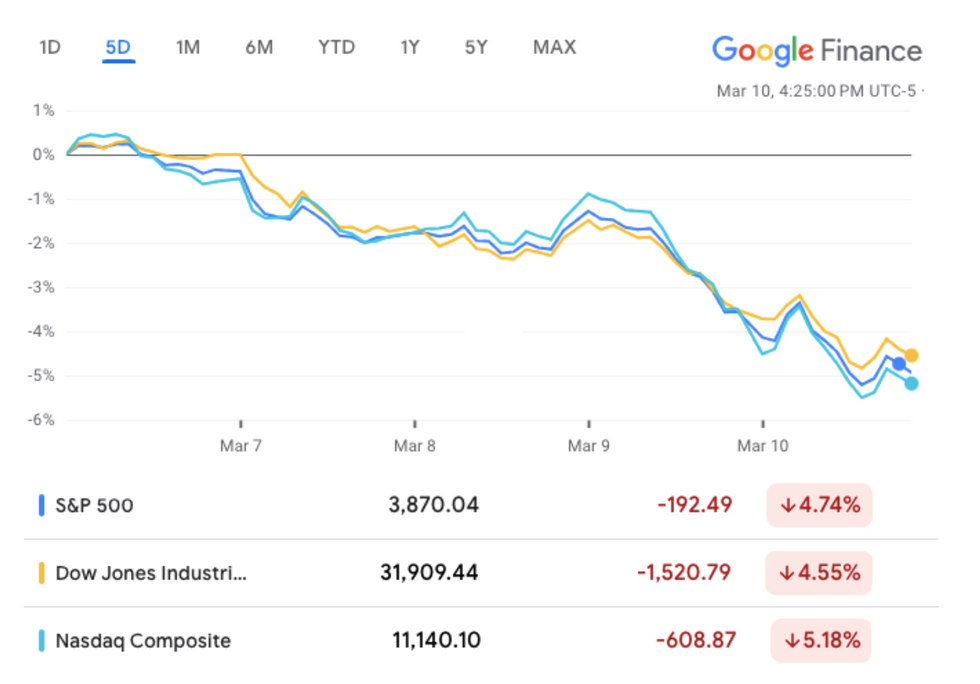

Last month Federal Reserve Chairman Jerome Powell seemed optimistic when he said that the U.S. was entering a “disinflationary process”, indicating interest rates would go up by smaller increments in the coming months. Investors shared his optimism but that has now all but evaporated. This week in testimony to Congress, Powell said that rates would go up by larger increments if data on inflation and jobs growth came in strong. Stocks fell in anticipation of rougher economic conditions ahead, and investors are finally coming around to the understanding that interest rates will not be cut in 2023.

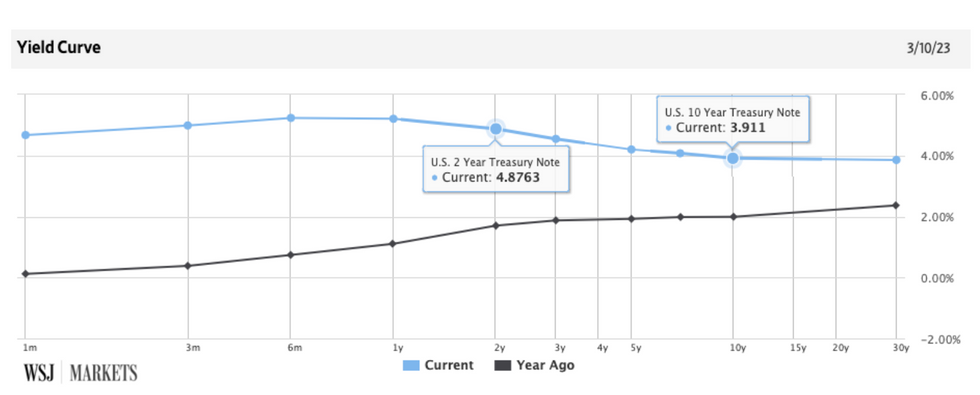

Bond traders reacted to Powell's testimony also. Selling was quick, and short-term Treasury yields jumped given how sensitive this market is to near-termchanges in interest rates. The yield curve, which is the plot of U.S. Treasury rates at different maturities, is inverted. Short-term treasuries are yielding more than longer-term. (Remember that when prices decline, yields move up.)

The bond market's crystal ball is predicting higher interest rates ahead, likely to be followed by a recession, followed by a rate cut by the Fed.

Corporations have not been waiting around to see what the latest is from Chairman Powell. Already this year businesses have done a lot of borrowing and bond issuance, taking Powell at his word and moving fast to borrow before rates get any higher. This is a shift from last year’s relatively normal activity.

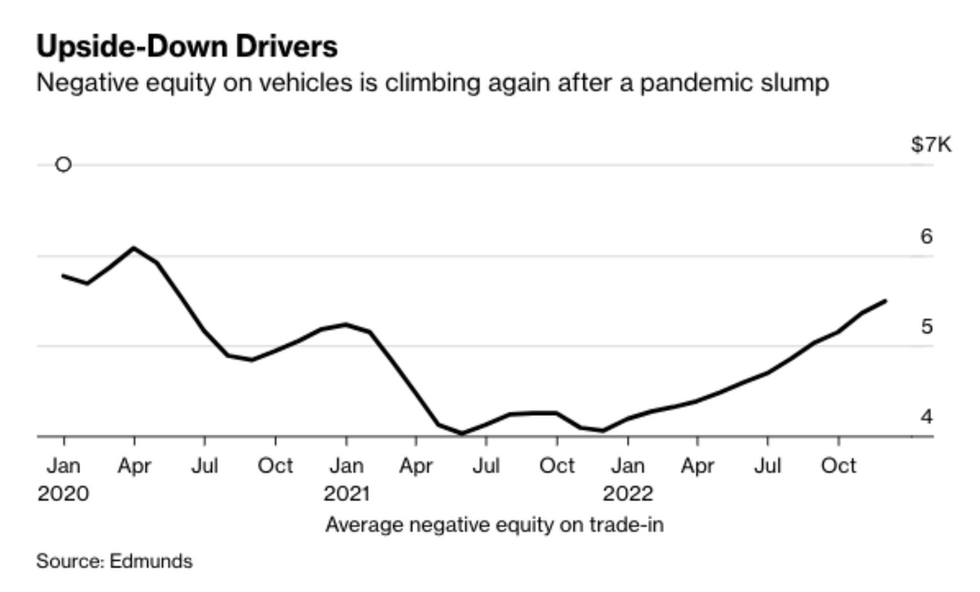

Americans are underwater on their car loans and part of the problem appears to be the desire to upgrade too frequently. Consumers are trading in cars that are worth less than their outstanding loan to buy a new one. Then they are re-financing the old debt along with borrowing for the new car, all at high rates. Loan terms are longer now too, at 84 months, or 7 years, as opposed to the previous norm of 5 years. Based on trade-in data, the negative equity is near $5,500 per Edmunds.

A strong link between North American companies and corporate board diversity is emerging. The more women, the better corporate and fiscal governance appears to occur, leading to higher financial credit worthiness. High-rated companies have an average of 44% women representation; low-rated firms have 15%.

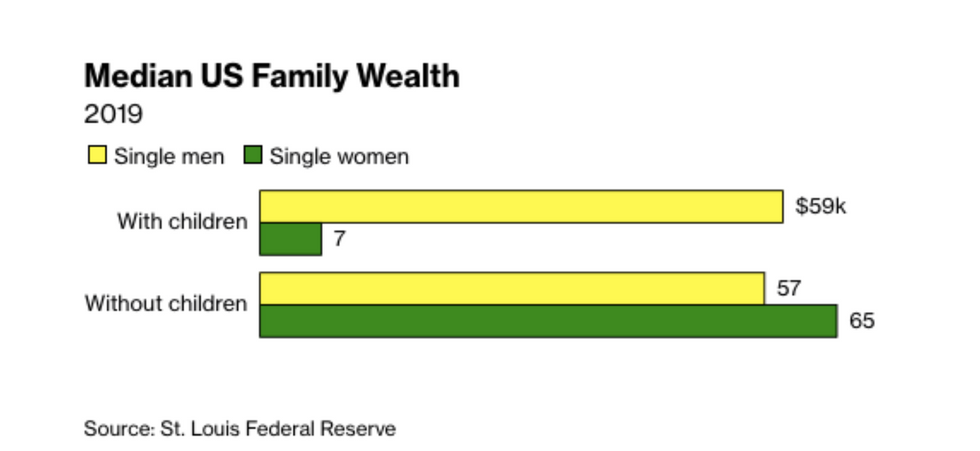

Unmarried women with no kids are seeing their net wealth surpass their male counterparts in the same demographic. They are also on track for retirement, right in line with their married cohorts who typically have the advantage of two incomes. This despite the tax code not being in their favor (single filers and child-free Americans pay more in taxes) and housing is more expensive on one income.Single-women with children are way behind the rest. Given that the last data is from 2019 and pre-pandemic, it is likely this number has gotten even more dismal.

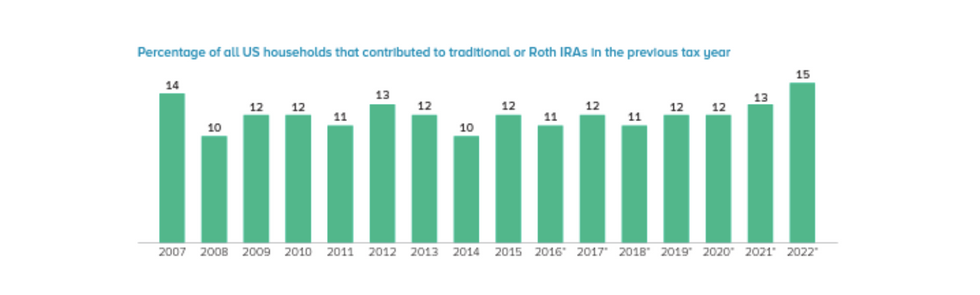

Paying Yourself with IRAs

A recent study by the Investment Company Institute found that IRAs are under-utilized. Most households do not regularly contribute to them even though this is an option for anyone who has earned income, or is married to someone with earned income. Just 15% of all U.S. households made contributions to a traditional IRA or Roth IRA for tax year 2021, and that’s actually the highest percentage in the last 15 years.

Ed Slott, an IRA expert and enthusiast, says that the accounts remain confusing and no wonder, Congress changes the rules frequently. How much you can contribute, income ceilings and and withdrawal rules have been shifting more frequently over the last 5 years. However, the contributory IRA remains the most accessible, tax-friendly and flexible retirement savings vehicle out there. Here’s a quick primer on the ins and outs. Given that it is tax time, and contributions to IRAs can still be made for tax year 2022, you do not want to

miss out on any savings opportunities.

Contributions to traditional IRAs can be made by anyone with earned income (a W-2 or 1099) in 2022. Even minors with earned income can have custodial IRAs. If one half of a couple does not work outside the home, they can still add money to an IRA in their own name; this is called a “spousal" contribution.

There are no income limits preventing one from making a traditional IRA contribution. However, depending on your total income and factoring in contributions to a 401(k), the ability to deduct your total contribution from your income may be limited.

There are income limits if you are considering contributing to a Roth IRA, see chart above. Otherwise the same eligibility rules apply - one must have earned income or be married to someone with earned income. Contributions are made after-tax but there are no further taxes on growth or distribution provided you follow some rules, including having the IRA for at least 5 years and being over age 59 1/2 at distribution time.

BUT, you can still get money into a Roth via the “backdoor” process. In this scenario, one makes a non-deductible contribution to a traditional and thenconverts it to a Roth IRA. The tax benefits are the best if there are not other significant traditional IRA assets. (Talk to your CPA about this!)

Spending in Pursuit of Love

If the pandemic did not dampen one’s enthusiasm for dating in the age of deadly viruses, inflation seems to be throwing cold water on the party. A 2022 survey from online dating site Dating.com found that over half of single people are holding off on scheduling dates in order to save on the effort and expenses that go into them – dinner, drinks and a movie are pricey but so are clothes and transportation. Instead singles are getting to know people better before splashing out a lot on a big night.

Match.com calls this “conscious dating”. Minglers are also changing up the usual routine. Meet-ups might now happen during the day, or over coffee, taking in an art museum or a park instead of a pricey evening event. Match.com’s surveyed singles showed that 23% are now more appreciative of frugality in a partner. One-third say inflation has made them more interested in finding someone who is financially stable. And nearly all, at 96%, agree that teaming up with someone who shares their financial philosophy is important, the highest it has ever been in this survey.

While “Netflix and chill” was an appealing invite for Covid times, it has lost nearly all of its appeal for the dating cohort. Dinner and a movie is back in vogue. But it’ll set you back a bit. The most expensive city for such an evening is New York City at $230. In Seattle it will cost $177 and $160 in Portland. But as a percentage of the average salary, such a date is most expensive in Las Vegas, where dinner and a movie costs $194 and is 17% of a week's earnings. Click here to see more numbers and the breakdowns.