.png)

Weekly Reflection for May 19, 2023

- Serene Point

- May 19, 2023

- 4 min read

The Week - An Update in Charts

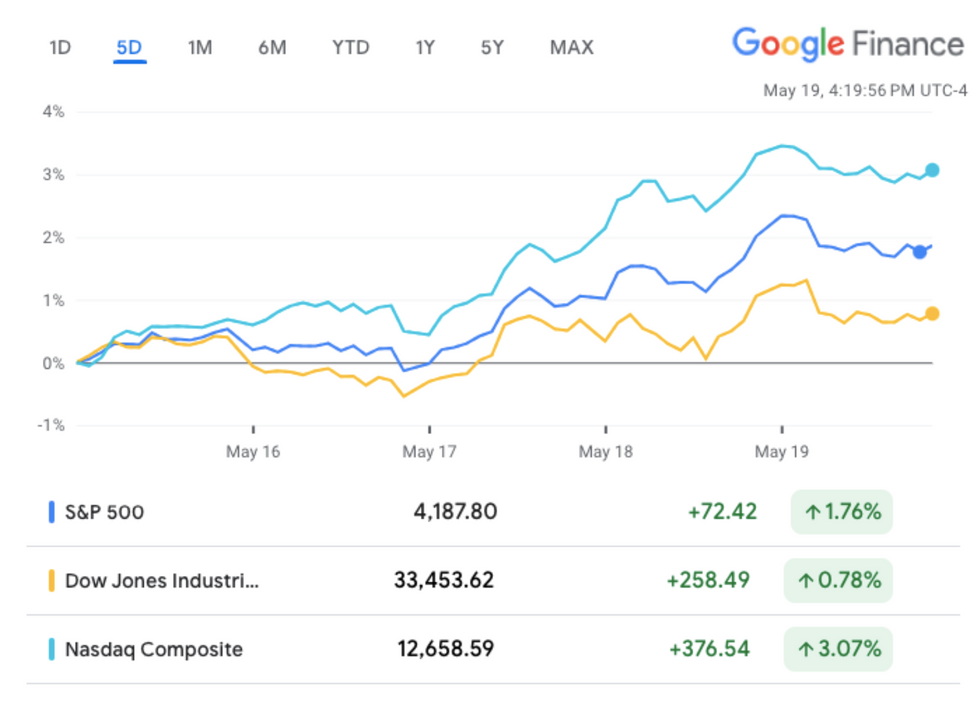

During a week when the U.S. debt limit talks dominated the economic world, the U.S. major indices ended trading on Friday with a whimper. Most of the week there was enthusiasm for a deal soon as the negotiating parties in Washington D.C. sounded upbeat. Also weighing on the markets is the strength of the economy - enough strength that the Federal Reserve might just consider a pause in raising rates, not a full stop. The Fed meets again on June 13th.

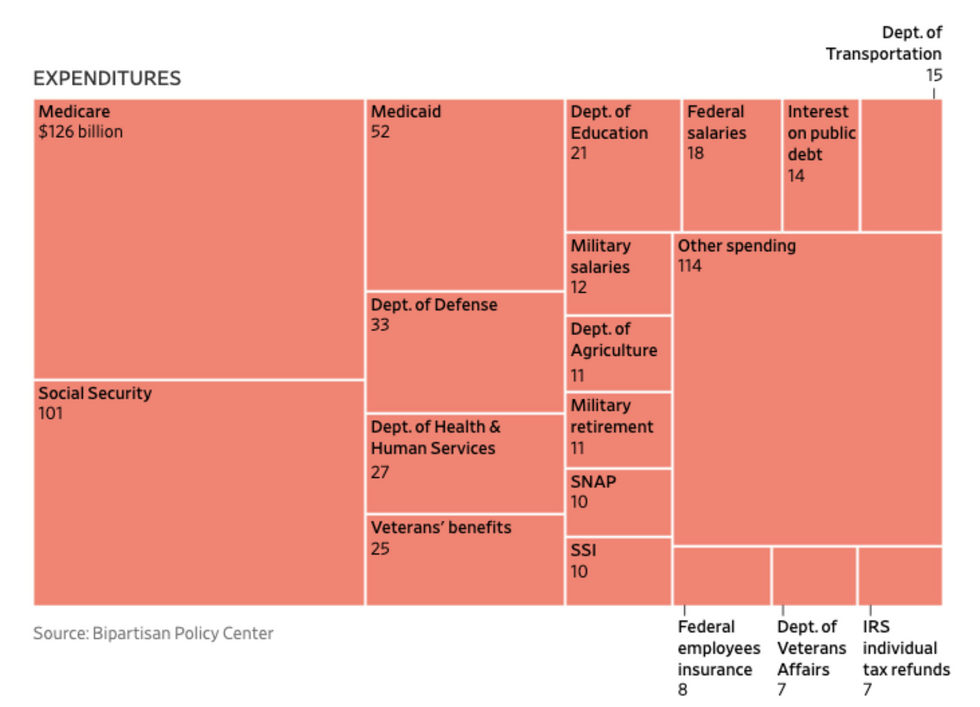

This fiscal year, which runs from October 1, 2022 to September 30, 2023, the federal government expects to spend about $1.5 trillion over what it collects in revenue.

In just the month of June, the government will collect $495 billion in revenue, but that will only cover 80% of its expenses, which total $622 billion.

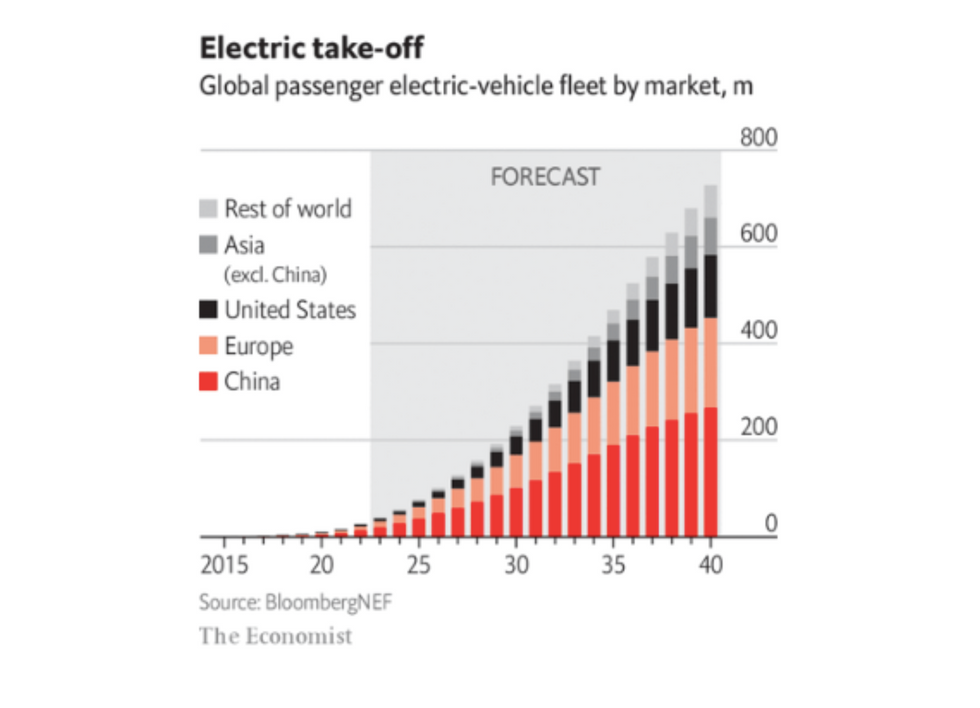

Tough regulations are pushing electric vehicle adoption in China more so than in any other region. China is requiring that 20% of cars must be new energy vehicles by 2025, just 2.5 years from now.

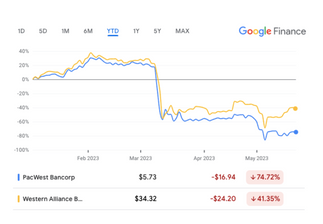

Call regional bank stocks the new "meme" stocks - ones that traders love to day-trade. The prices of both PacWest Bancorp (PACW) and Western Alliance (WAL) have declined massively year-to-date as many predict both may go the way of Silicon Valley and First Republic banks - bust.

This has attracted risk-takers, like those who trade other near death stocks like Hertz, GameStop and AMC Entertainment. The high volatility and volume can turn into big profits, or losses, for those who are willing to jump in. Both stocks finished up this week, but have huge losses on the year.

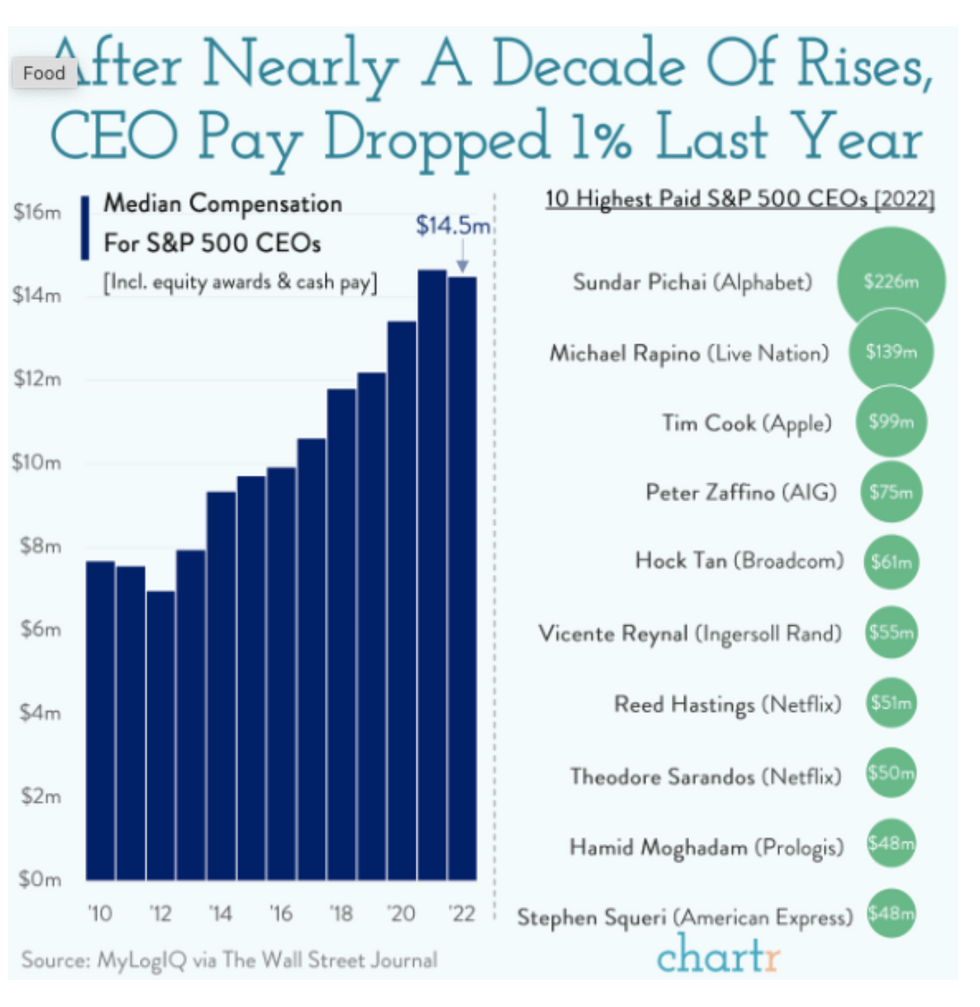

The stock markets dropped double-digits last year but that did not budge the pay of highest paid CEOs. One exception is Elon Musk, arguably the most famous CEO in the world these days. Not only did he lose $10 billion in net worth due in 2022 to Tesla's drop, he has not taken a paycheck since at least 2020.

Homeowners Embrace “Quiet Quitting”

This is according to real estate brokerage site Redfin and its chief economist Daryl Fairweather, who posted the comment on Twitter recently.

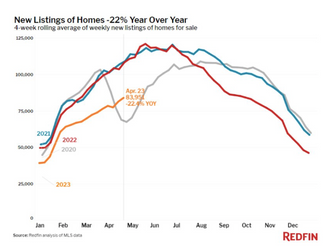

New listings have fallen 20% from a year ago, just as real estate’s busy season is set to kickoff. No one really blames homeowners who express concern about losing their low interest rate mortgages, which rarely can be converted to another new property and mortgage. So they are sitting on their hands, staying with the property they have for now.

Residential real estate remains a seller’s market with intense demand however housing prices are coming down, if only a bit. The median home sale price is near $372,000, down 2.7% from May 2022. (Price drops are much larger in the big cities – down 13-16% in the Bay Area and nearly 18% in Austin.)

New homes are doing better than used. The prices for new construction have barely budged over 2022, clocking in at $398,000. Mortgages are still in the 6.7% range for a 30-year term and experts say they will have to get closer to 5% before a balance between sellers and buyers can be found. One way to measure balance is to consider supply. Right now it would take 2.5 months to sell all of the inventory available. Four to five months is the sweet spot, according to the National Mortgage Professional industry group.

The Fall of the Zombies

You know you are a financial zombie if you have debt but your income does not cover even the interest payments on the debt. You then have three choices – find a way to make more money, refinance your debt to a morereasonable amount or go bankrupt.

We do not refer to struggling individuals as zombies but we definitely use the word to describe businesses that stagger around long past one's useful life. They are a drag on the system, tying up people, money and other resources that could be better used elsewhere.

Zombies eagerly took bailouts offered via government stimulus in 2020 and 2021 and were able to prolong the inevitable a bit longer. Experts warned as soon rates increased, the debt burden would close in on them again. That time is upon us.

Between last Sunday and Monday, a remarkable seven sizable companies filed for bankruptcy using Chapter 11. (This is the “reorganization” option, versus Chapter 7 which is full liquidation.) Some of these companies are publicly-traded, like Athenex (ATNX) and Monitronics (SCTY), which is better known as Brink’s Home Security; this is Monitronics’ second go with filing Chapter 11. Others that filed this week received millions of private investor money like Cox and Venator Materials. Those assets will likely all be wiped out.

Envision Healthcare, a physician staffing company, is a great example of a zombie that survived the pandemic only to die once it was declared over. Back in April 2020, Envision announced they were considering bankruptcy; by June, a lifeline it could not have predicted, arrived in the form of a $60 million forgivable loan via federal Covid-19 emergency funding. Last September Moody’s warned again about the company’s health and on Monday it filed for bankruptcy.

Now that cheap money is unavailable, expect more bankruptcies to come. It could be a slow wave that drags on for years as companies always try to raise more cash, restructure or sell off assets to avoid the dreaded bankruptcy court.

By April, the last full month of records, corporate bankruptcies had totaled 236, which is the most since 2010. Among the notable names and businesses are Bed, Bath and Beyond, Serta Simmons Bedding, Silicon Valley Bank and Party City.

It is hard to find a company anymore that has no debt. In the last 10 years, very few companies have passed up the opportunity to borrow at near-zero rates. A quick look at the companies in the S&P 500 indicates that every single one of them has loans outstanding, whereas a few years ago there were at least a dozen or so that were debt-free.